See Who Supports Our Campaign

At XTB, we believe that financial independence should begin when young people start shaping their futures.

By empowering young investors to take control of their financial journey earlier, we can help build a stronger culture of saving, investing, and financial confidence across the UK.

We’re asking the UK Government to reduce the minimum age for independently opening and managing an ISA from 18 to 16-years-old.

This simple change would bring the ISA rules in line with other key milestones of adulthood leaving school, starting work, and (soon) voting.

Our goal is to give financially aware and motivated young people the freedom to begin their savings and investment journey sooner, helping them build healthy habits and long-term financial security.

.png)

.png)

.png)

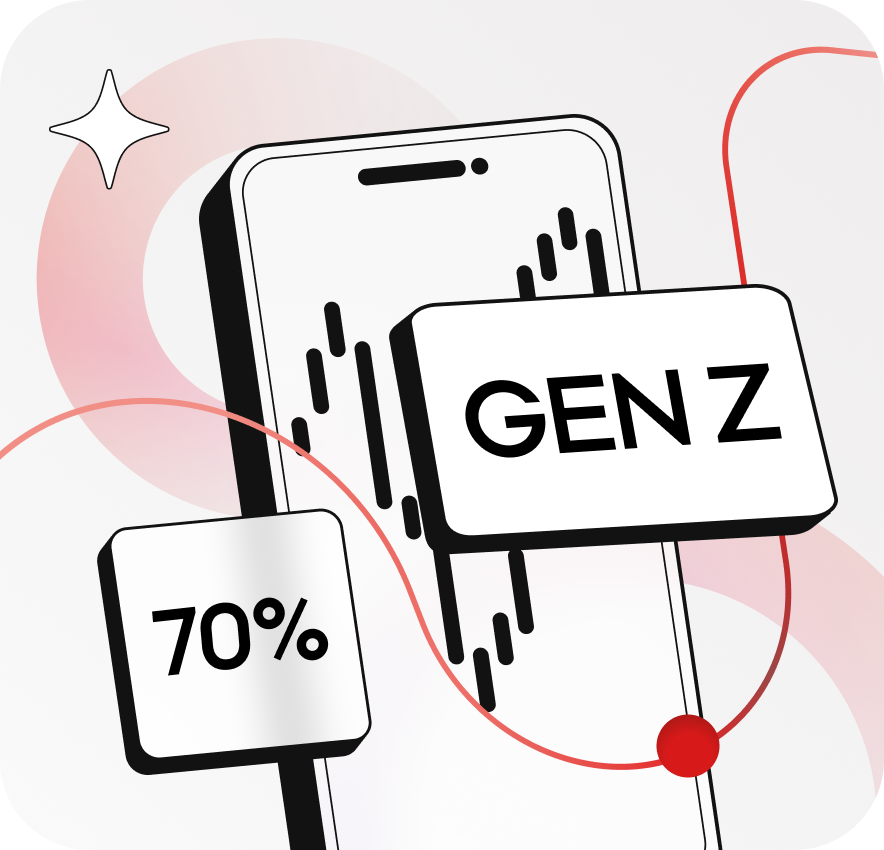

70% Gen Z ISA holders believe 16 and 17-year-olds should be able to invest in a Stocks & Shares ISA.

Majority of parents think their children aged 16 and 17-year-old should be allowed to invest their own money in an ISA.

Source: Find Out Now on behalf of XTB

.png?width=915&height=880&name=KV_LP_Majority%20of%20parents%20ISA_2025_884x850%20(1).png)

ISAs have long been one of the UK’s most successful and trusted savings and investment products. They allow people to save and invest tax-free, building financial security over time.

By extending ISA eligibility to 16- and 17-year-olds, we can:

Help young people develop positive saving and investing habits early.

Support financial education and literacy among the next generation.

Align the financial system with the government’s broader ambition to create a nation of savers.

ISAs are also low-risk investment vehicles. They don’t allow leveraged trading or complex strategies just straightforward investing in regulated global stocks and shares. This makes them an ideal starting point for those learning about responsible money management.

Right now, under-18s can only access a Junior ISA (JISA) — a great tool for parents saving for their children, but a limited one for young people ready to manage their own money.

Here’s the problem:

The annual JISA limit is £9,000 less than half the £20,000 available in an adult ISA.

The young person cannot withdraw funds or manage the account until they turn 18.

Financially independent 16 and 17-year-olds who work or save are restricted from managing their own investments.

This campaign is about giving every young person the tools, access, and confidence to take control of their financial future.

The key benefit of an ISA is its tax-free status. Any interest earned on ISAs or any capital gains or dividends generated within the Flexible Stocks & Shares ISAs are completely exempt from UK income tax and capital gains tax.

Earn 4.25% (variable rate) interest on GBP on your uninvested funds. Interest is calculated daily and paid out monthly.

At XTB, we believe great investing starts with great education. That’s why we offer free access to eBooks, articles, videos, webinars, and expert market analysis all designed to help customers of every age grow their financial knowledge.

We’re also committed to supporting young savers at the start of their journey. If adopted by the UK government, XTB’s proposed educational programme will provide free, innovative learning resources to help young people build confidence, independence, and smarter money habits.

Regular news stories and campaign updates.

For more information about the campaign, please contact press@xtb.com

.png?width=425&height=442&name=MWC_KV_LP_Main%20KV_UK%20(1).png)

XTB is a global fintech company that provides individual investors with instant access to financial markets from around the world, through an innovative online investing platform and the XTB mobile app. Founded in Poland in 2004, we support over 2 million customers globally in achieving their investment and trading ambitions.

At XTB, we are committed to the continuing development of the online investing platform enabling our customers to access 10900+ instruments.

Our online platform is a top destination not only for investing but also market analysis and education. We offer an extensive library of educational materials, videos, webinars and courses to help our customers become better investors, irrespective of their trading experience. Our customer service team provides support in 18 languages and is available 24/5 via email, chat or phone.

In over 20 years of operation in financial markets, we have established 12 offices worldwide including Poland, the UK, Germany, Romania, Spain, Czech Republic, Slovakia, Portugal, France, Dubai and Chile.

Since 2016, XTB shares have been listed on the Warsaw Stock Exchange. We are regulated by the world’s largest supervisory authorities: Financial Conduct Authority, Polish Financial Supervision Authority, Cyprus Securities & Exchange Commission and Financial Services Commission.

Visit https://www.xtb.com/en for more information.

To lower the age at which an individual can open ISAs from 18 to 16-years-old.

To empower a younger generation to save and invest for the future and bring the age

limit in line with other milestones such as minimum age for leaving school, starting work and (soon) voting. XTB and others want to help kick start an investing culture among the youth as early as possible which aligns with the government’s ambition.

Not every 16 and 17-year-old will want to open a Stocks and Shares ISA, however those

who are interested in investing, who have financial independence or want to learn about the stock market should be allowed the same benefits as anyone of 18 years or older.

JISAs are a great vehicle for parents to save for the children - in their children’s names.

However, the annual deposit limit is just £9,000 rather than the full £20,000 which can go into an adult ISA and there are strict controls on what the owner or controller of a JISA can do until they are 18. The most onerous being that they cannot withdraw any money. It makes no sense to limit a 16 or 17-year-old’s access to money if they are earning and/or supporting themselves.

We fully accept that not every 16 or 17-year-old will be interested in investing, however

many of the most successful investors and entrepreneurs start at an early age. If we

want to create an investment culture in the UK we believe it is key that we start early,

educating and offering opportunities to those who show an interest. It will also enable for

young people to develop life skills through the learning about and management of

money, which helps to instil discipline from an early age.

No, the principle is to offer the same opportunities to 16 and 17-year-olds as are

currently offered to 18-year-olds. We want to empower young investors by educating

them about risk as well as exposing them to the potential rewards of saving and

investments.